A Project on the prediction of systematic risk in stock market based on multibranch LSTM model with multidimensional heterogeneous perspective

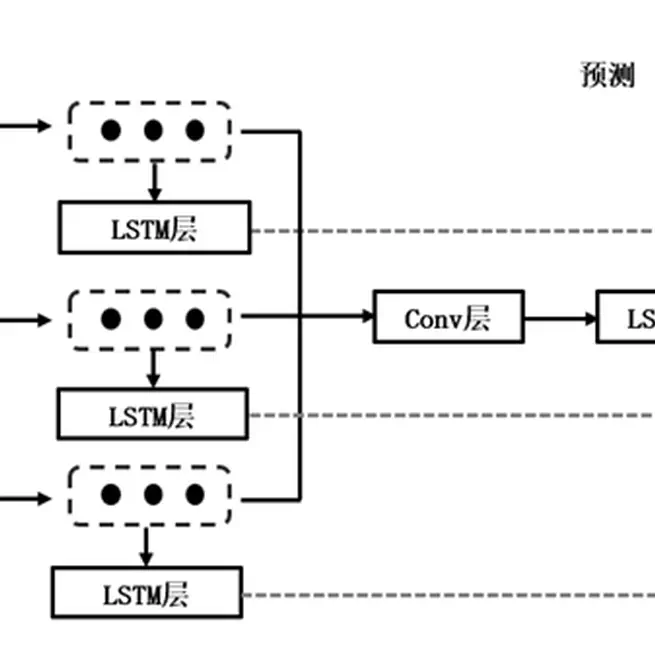

This project adopts multi-dimensional, heterogeneous data—covering contagion effects, textual information, and fundamentals—to construct a feature set. Contagion indicators are derived from global market indices, capturing inter-market risk structures and CoES-based correlation vectors. Text features come from A-share financial news, while fundamental indicators encompass macroeconomic, stock market, and foreign exchange data, plus historical systemic risk. A multi-branch LSTM model is then proposed to predict systemic risk in the A-share market. Three independent LSTM branches extract information from each modality, and a separate convolutional-LSTM branch learns holistic knowledge. Results show that contagion-network features significantly enhance model performance, and the multi-branch LSTM effectively supports the monitoring and early warning of systemic risk in the stock market.

Dec 1, 2023

Prediction of Enterprise ST Based on LSTM+GRU

The research aims to predict the likelihood of enterprises being classified as "Special Treatment" (ST) in the upcoming quarter using machine learning (ML) and deep learning (DL) techniques. The focus is on enhancing financial distress prediction by incorporating novel indicators beyond traditional metrics.

Aug 22, 2022